If you’ve received a paycheck through direct deposit or scheduled a recurring payment from your bank, you’ve used Automated Clearing House (ACH) processing. ACH transactions are more common than you might think (with fast-growing adoption!), and are a cost-effective way to send and receive payments electronically.

What is ACH Processing?

ACH stands for Automated Clearing House, which is an electronic network of financial institutions across the United States. It provides the ability to directly debit (think: bill payment) or credit (think: direct deposit) a consumer or business bank account, simply by using their routing or account numbers. The ACH Network is managed by NACHA, which provides governance and regulation over the Network.

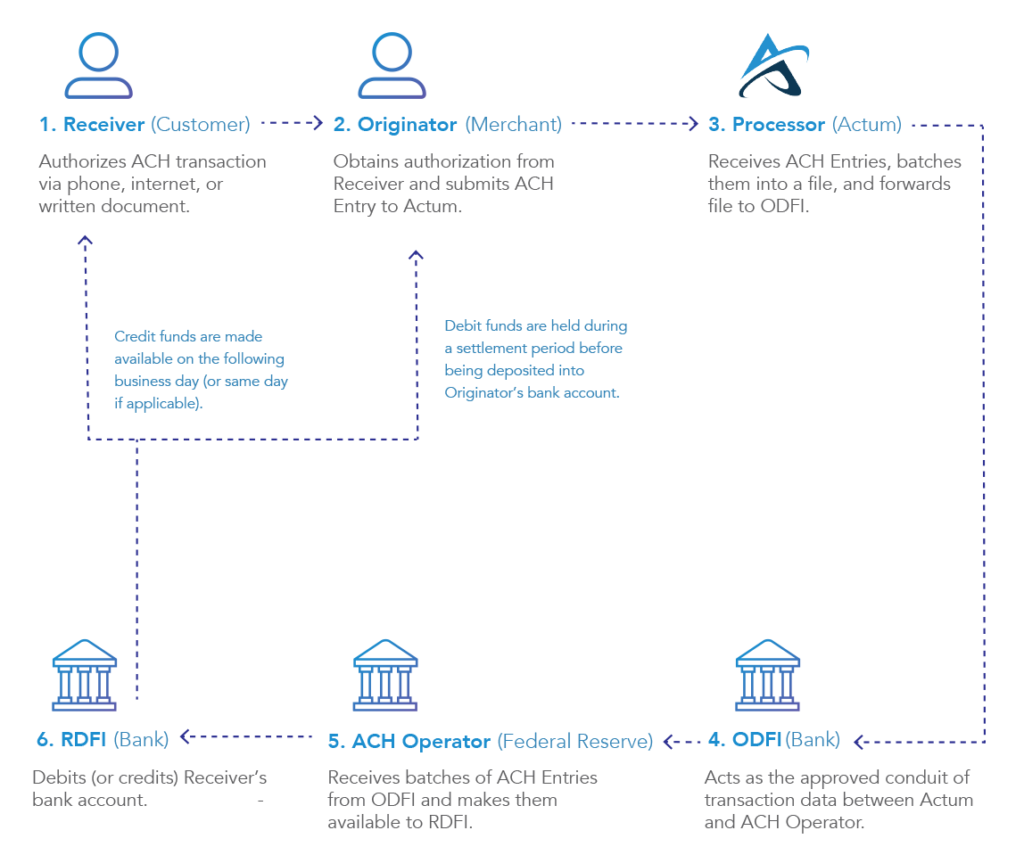

In ACH, there are Originators (e.g., Merchants) and Receivers (e.g., Customers). There are also ODFIs (Originating Depository Financial Institutions) and RDFIs (Receiving Depository Financial Institutions). An ODFI is the financial institution that the ACH transaction starts or originates from. An RDFI is the financial institution that receives the ACH transaction.

ODFIs transmit transaction data to the Federal Reserve (or the Electronic Payments Network) which acts as an ACH Operator between the ODFI and RDFI.

How does ACH work with Actum?

Not all banks have the infrastructure in place to fully offer ACH Origination services to their banking customers. In most cases, an intermediary, or a Third Party Sender, with an established account at an Originating bank (ODFI) will process ACH Entries on the Originator’s behalf.

Actum acts as a Third Party Sender, providing an easy “on-ramp” to the ACH Network. We leverage relationships with multiple banks to ensure timely originations of all transactions.

As a Third Party Sender, Actum allows your business to act as a processor by extension, so that you can collect, transmit and reflect data with ease. Actum manages the actual funds and banking relationships for you, which eliminates the headaches of underwriting new accounts, risk monitoring, managing returns, handling payments-related customer service tickets, and building out complex accounting and compliance management systems.

Settlement Periods and Payouts

It’s important to recognize that ACH is not considered a real-time payment method. Our standard settlement cycle for most ACH debit transactions to post is three (3) to five (5) business days.

Like paper checks, ACH payments can be returned for a number of reasons, including invalid account numbers, inability to locate account, chargebacks, and non-sufficient funds (NSF). In any of these cases, the transaction will have failed. As long as it is not returned during the settlement period, funds will be deposited into your bank account.

Payments can be submitted at any time and, through Actum, can be processed as soon as the same day. Also, Actum offers late night and weekend processing. This means that we keep payment submission deadlines pushed out later than other processors so you can submit more transactions on the same day to shorten your settlement time.

For qualified merchants, Actum also offers an Accelerated Payouts feature that can help shorten your settlement time to receive payouts in two (2), one (1), and sometimes even zero (0) business days.

What does ACH Processing look like?

To help you visualize key players and processes involved in an ACH transaction and their associated roles in context, we’ve created the following high-level illustration:

Figure 1: The ACH Processing Flow with Actum

How can merchants benefit from ACH?

The following are some examples of how using ACH with a Third Party Processor can benefit your business:

- Cost savings: ACH transaction fees for debit and credits are typically lower than credit card fees.

- Automated recurring payments: Using ACH for recurring billing provides added convenience to consumers.

- Flexible payment options: By adding ACH as a billing option, merchants can increase retention rates.

- Brand continuity: Using our white-labeled API helps maintain brand recognition.

- Bank verification: With options like pre-notes, micro-deposit validation, and Authentecheck auto-verification, customer bank accounts (and balance amounts) are instantly verified for ACH transactions.

Why Actum?

It’s easy to set up and manage one-time and recurring payments using our web portal, powerful API, or batch upload method. Our advanced software also allows merchants across all industries to originate, track, and pull reports on submitted electronic transactions. Our API can also integrate seamlessly into new and existing systems. You can learn more in our Guide for Software Companies.

To minimize risks, we adhere to stringent, industry-standard compliance policies and procedures, with data protection as a top priority. We encrypt all payment data during transactions, and offer the option to tokenize bank account numbers— thereby minimizing concerns around holding onto sensitive financial data.

Actum is frequently recognized for our 20+ years of hands-on ACH expertise and client-focused support team. To learn more about ACH and working with Actum, we invite you to Contact Us.